Well, I don’t want to talk about any specific company. I’m just making a general statement that we think competition is good. It makes us all better. And we are ready to suit up and go against anyone. However, we will not stand for having our IP ripped off, and we’ll use whatever weapons that we have at our disposal. I don’t know that I could be more clear than that.

Tim Cook, my favorite Apple exec, in January 2009.

One thing should be obvious: the accusations against HTC are aimed at Google and Microsoft or more broadly still, they are aimed at any mobile software competitor that intends to use touch and gesture inputs.

When Jobs said in 2007

We’ve been pushing the state of the art in every facet of this design. We’ve got the multi-touch screen, miniaturization, OS X in a mobile device, precision enclosures, three advanced sensors, desktop class applications, and the widescreen video iPod. We filed for over 200 patents for all the inventions in iPhone and we intend to protect them.

he implied that Apple had approached this new input method with much more care than when they introduced the mouse and windowing interfaces in 1984.

Unlike the fight over Windows, which was a copyright debate, this will be all about patents. Apple ultimately lost the GUI fight over the MasOS windowing interface, which is why I think they are much more prepared this time.

Given this strategic intent, the only questions were how the war would be engaged and on what terms. A few skirmishes caused some head fakes.

First, came apparent threats against Palm. Apple was certainly debating going after Palm, but I think they realized it would not be a good strategy. Mostly because the signal would be weak. There would be few consequences to Palm being punished. Palm’s integrated model is not employed by many of the larger device vendors. Except for Nokia, all other vendors license their OS, Samsung, LG, Sony Ericsson and Motorola would not be infused with anxiety over Plam taking a hit.

Second, came the pre-emptive attack from Nokia. Apple was not ready to go after Nokia last year because Nokia did not yet have a UI “worthy of being infringing”. In other words, there was no target to shoot at. Nokia’s suit was pre-emptive in that it centered on their desperate wish to have a cross-license agreement–trading GSM patents for touch patents.

That skirmish should not detract from what’s the real goal here: securing monopoly rights to mobile computing interfaces.

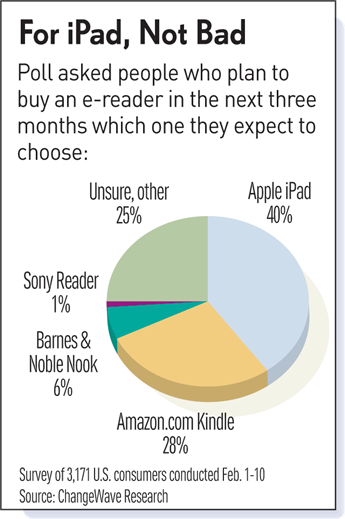

A survey of nearly 3,200 consumers by ChangeWave Research finds that 40% of people planning to buy an e-reader in the next 90 days expect to get Apple’s iPad. The current leader, Amazon.com’s (AMZN) Kindle, came in second at 28%.