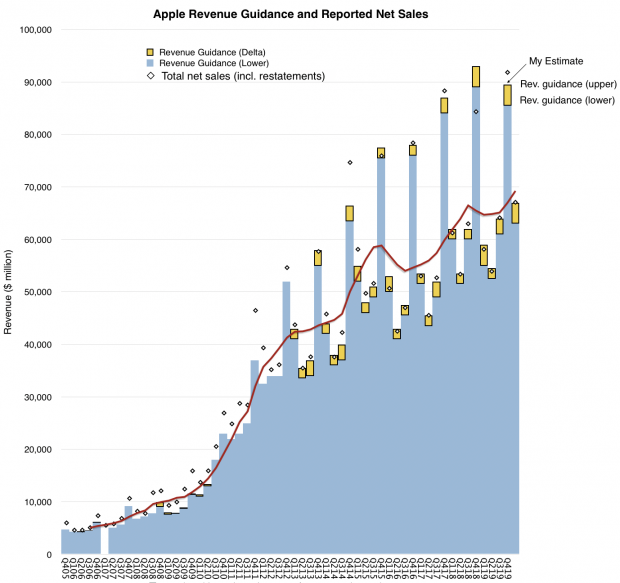

Exactly one month ago Apple reported their highest quarterly revenue ever. They also guided to growth of between 8.6% and 15.5% into the current (1st calendar) quarter. This guidance is illustrated as the right-most bar in the following graph:

Note that the growth is relative to the year-ago quarter. The quarter was almost a third over by the time the issuance of guidance but less than three weeks later the company withdrew their guidance. The company did not issue new guidance.

The reasons given were both a restricted supply and a disruption in demand due to the COVID-19 viral outbreak. That outbreak paralyzed China and in the 10 days since has come to threaten the world.

Apple was the first company to warn about the impact of the virus on its business but not the last. The market reaction was muted. Mysteriously, the market seems to be reacting to the outbreak at this later time even though the dynamics of the epidemic were foreseeable.

The question of impact on the business is still open but I’d like to reflect a bit on the impact of any number of possible disasters or “acts of God” on any business.

The greatest catastrophes in history were wars and pandemics. In the 20th century in particular there were two world wars and one large pandemic in 1918. Add to that a depression and you would think that century was cursed.

And yet, these crises merely delayed technologies. They did not eliminate them or the companies which introduced them. For example, the introduction of Television was delayed by WWII and the adoption of the automobile was paused. At the same time new innovations were introduced including plastics, radar and microwaves and jumps in manufacturing productivity. The 1918 flu was followed by the roaring 20’s and WWII by the post-war boom years. The 20th century came to be celebrated as the most innovative time in history, a time when standards of living and prosperity exploded.

It’s not prudent to ignore a pandemic but it’s not prudent to contemplate an apocalypse will follow. Demand deferred is not demand destroyed. Civilization is fundamentally able to absorb these shocks and it’s useful to look to history to see exactly how we managed to do so.

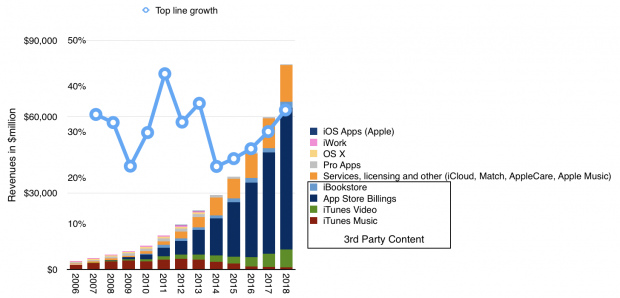

During 2016 Apple services revenues were $25.6 billion. In January 2017, just after the end of that year, Tim Cook said “We feel great about this momentum, and our goal is to double the size of the services business in the next four years”.

If Apple were to hit that target, during calendar year 2020, Apple’s services revenues should exceed $50 billion. In 2017 they were $32 billion, in 2018 they were 41.5 billion and so far this year they are 23 billion. If, as has been the case during 2017 and 2018 (see graphs below,) Apple were to maintain 30% growth in Services during the rest of this year they will have revenues of $51 billion in 2019; reaching the doubling tarted a year sooner than predicted.

Apple will have doubled Services in 3 years to a level equivalent to a Fortune 63 company (right behind Goldman Sachs).

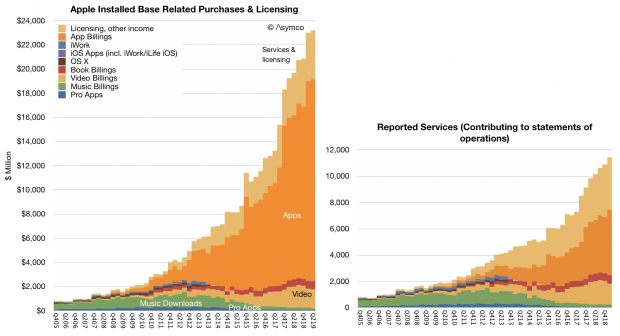

Keep in mind that the reported revenues are not billings or what consumers actually spend. That figure is at a run rate of over $71 billion. You can see the difference between billings and reported revenues in the graphs above.

So what made this possible and what is the source of growth in the future?

As my estimates above show, the growth came from apps and licensing and other revenues. Apps include many third-party subscriptions and licensing includes Google TAC and other income includes Apple’s own subscription services and a few additional items like Apple Pay, AppleCare and iCloud.

What Apple is launching this year will boost this even further with TV+, Card, Arcade and News+. These are a new set of specific services that, apart from Card, will require subscriptions and will deliver Apple-specific content. Unlike previous Music and TV offerings, what Apple has embarked on is a high degree of involvement in the content creation process. These will be Apple TV shows, Apple video games and Apple-directed News feeds.

This is quite the watershed moment. Apple, a company dedicated to providing tools to content makers and content consumers, choosing to be involved in the lottery-like game of choosing and backing winners in creative works.

Can a company with good taste about devices and software successfully extend that capability to content? That seems to be the question many are asking: How good is Apple at creating hits? The process of hit creation is difficult but it’s not completely random. There are many individuals who have skills or taste. And Apple’s approach seems to be to hire people with such skills. These “executives” then proceed to attach people with great track records in hits and who may have the star power to attract audiences. It’s not a matter of complete guesswork. It’s actually the approach most “streamers” have: They hire studio executives, attach talent to projects and spread bets.

This is why there has been a rush by streamers to secure programs and A-listers. There might be a variety of subscriptions users are likely to pay for but there is a fixed number of bankable names in the business.

But let’s pause here to think more deeply about what is happening. Without much notice, we are seeing a content world where distributors are locking up talent and creating a studio model where production, talent and distribution and display are under one roof. This is exactly where the movie industry was in the so-called golden age of Hollywood. The era of the studio system. An era that ended with divorcement—the complete separation of exhibition interests from producer-distributor operations or the forced divestiture of theaters by production/distribution.

Another observation to be made is that the bundling and binding of content into specific distributors creates a walled garden effect. This extends beyond video content to games (a larger business than film, at least at the box office, see below) and to apps. Arcade games are Apple-exclusive. Many apps which depend on Watch, AR and other unique technologies become exclusive, and of course unique titles.

As far as consumers are concerned this might be just fine. There are very implicit lock-in effects of ecosystems, from UX muscle memory, switching costs for data, network effects from friends/family/co-workers in the same system. The extension of this to cultural content, news curation, music curation and privacy curation could be the comfortable default for many.

In this world-view the proposition Apple offers is very attractive. Look at the preference vacationers have toward packaged experiences. Look at the popularity of cruises. Look at the way features are packaged in cars. Look at meal delivery and the packaging of ingredients into something you can cook at home. Look at fitness and the packaging of instruction with the exercise venue. The examples are plentiful.

A garden is lovely after all. The walls are there to keep danger and chaos away as much as to keep you in it. The constraints simplify as much as they restrict. Though it may be contrary to some modular and interoperable utopias which paralyze with choice, we might well be experiencing a triumph of the walled garden.

InstantDomains.com is the fastest domain search tool ever built, you can search domain availability for all 500+ domain extensions in milliseconds. Results load instantly and with an incredibly friendly user interface it’s easy to scan through which domains are and aren’t available.

A domain name generator additionally suggests alternative domains to the one you’ve searched for and you can filter results by 55 different industries to make results even more relevant.

Instant Domains works in 32 different languages and will display the most relevant and popular domain extensions based on your location.

If you’re in the market for a more premium or brandable domain you can search domains for sale with results in milliseconds.

Instant Domains will quickly become you’re favourite tool of choice for domain name searches and availability checks. Try it out now.

The old cliche is that we were promised flying cars but ended up with x where x is something trivial or mundane. Perhaps the best “x” is “140 characters”. This statement is meant to de-value the technologies developed in the last few decades. Instead of building grand things, we build trivialities. The irony is that x is often wildly popular and ubiquitous. x also generates a lot of profits and is likely to change behavior. Indeed, the flying car alternatives are almost always better ideas.

Flying cars are an example of “extrapolated technology” where we take a trajectory of improvement and expect it to continue forever. x are examples of “market creating” technologies which create new behaviors and which allow more people to do more things that they could not do before.

The flying car dream comes from a century of improvements in cars, and airplanes. The idea that cars must continue to get better and flying must come to personal transportation. When they are faster than what roads and human reaction times can allow and when they have more space than we can fill and when they have more cupholders than we can drink from it’s time to look for a new domain–the sky–for them to enter.

The alternative is literally unthinkable to the extrapolator: that we might drive less or not at all.

The promise of super-fast computers on every desktop and every living room of the 1990s is countered by an acceptance of a computer in every pocket and a tablet in every living room in the 2010s.

So in many ways the grandest technological revolutions are a study in humility rather than ambition.

Humility as a business model or as an operating principle is one of, if not the most most powerful tools for a manager . The queen of the virtues is most elusive but most enabling.

And so here we are, the Apple Card has arrived. And the Apple car hasn’t. The contrast is deliciously ironic. The cynics are out and having their fun. The users are out ordering the product. The cycle repeats.

Except the Apple Card demands explanation. It’s not explained by Apple sufficiently. It sounds like a slightly easier credit card. Perhaps a bit easier to keeps tabs on, perhaps a bit easier to manage payments and easier getting bonuses. It sounds, well, easier.

But easier doesn’t rock anyone’s world, they say.

It’s just another card, they say.

How can this change anything?

Here’s the thing: follow the integration. First, Apple Card comes after Apple Pay, more than 4 years ago. Apple Card builds on the ability to transact using a phone, watch and has the support of over 5000 banks. Over 10 billion transactions have been made with Apple Cash. Over 40 countries are represented.

I am quite sure Apple considered their card entry at the same time they considered Pay entry. The extension to a credit instrument is only logical as an addition the the Wallet.

The emphasis is on convenience, ease of use, integration and assistance. It’s what a credit card should be if you invented it today.

The application process is easy. It’s designed for the iPhone. No delays, no paper, no signatures.

It promises “A healthier financial life” through help in understanding your spending and acting on it. The goal is not to keep users in debt but to keep them loyal. Think about the asymmetry here.

The partner, Goldman Sachs, is chosen for their willingness to also align on incentives.

But more than anything the release of the Apple Card brings into question what could be next. The Card may not have been on everyone’s mind four years ago when we first saw Pay.

Now the die is cast. Apple’s goals seem to include enhancing financial and physical health. These are mundane goals, perhaps.

“The essence of ultimate decision remains impenetrable to the observer – often, indeed, to the decider himself.”

John F. Kennedy

The fact that we ourselves don’t know how we make decisions has not stopped us from proclaiming, loudly, that we know how everyone else decides. Such proclamations about others’ decisions are especially confident and assured the more important, or highly visible, the decision.

This is at the heart of analysis for large companies, especially Apple. The premise that decisions on product, positioning, investment and a myriad other necessary functions are guided deliberately through the will of single individuals in positions of power; rational single Actors that are directed by some rational, typically economic, calculus is pervasive. Without pause, we assume that analysis consists of de-compiling the calculus of that single Actor.

The diversity of opinion on Apple stems from disagreements about whether the calculus is purely economic or some other—aesthetic, virtuous or greater good, “satisfaction maximization” or something else that motivates the Actor.

However this is not the only decision process. It is in contrast to two other decision making processes: the bureaucratic model where decisions are the result of analysis of constraints, resulting in a “best compromise” between multiple sub-problem solutions.

Or the “political model” where maneuvering between factions with fractional power results in a consensus decision based on a political (zero-sum?) calculus.

One could classify these decisions processes as Graham Allison did in “Essence of Decision: Explaining the Cuban Missile Crisis“: The Rational Actor, The Organizational Process or the Governmental Politics models. That landmark work opened our eyes to the variety of ways organizations—not just governments—decide. It clashed with, to the point of refuting, the economic rationality model typically attributed to Milton Friedman.

When reading commentary on Apple decisions I almost always hear the causality ascribed to the “Rational Actor” model where the Actor is a person of great importance. The importance imparted upon them implicitly by being a “visible” person. That visibility comes from having been put forward by the company itself. We know of the Apple Actors as those whose names are revealed and we assume that those not visible are not Actors.

But, of course, visibility is a design. The company, known for its design, takes that ethos to its communications, and communicating who is visible and thus who is “an Actor” is a design decision. So we are led to believe that decisions are made by the Actors and who the Actors are is determined by the very entity we are trying to analyze.

Do you see the problem?

Rather than take the comfortable road and analyzing Apple by the surface that is exposed, the better approach might be to toss the Rational Actor model and think about the Organizational or the Political Models.

How does the company process information? How does it generate consensus? How does it deal with motivating employees? How does it allocate resources? How does it evaluate productivity? How does it balance morale and turnover? These are what Clay Christensen classified as “Processes” rather than “Resources” questions. The Actor model assumes all decisions come from individuals who are, in a large organization, Resources. They come and go. They can be hired and fired.

The Political model asks further if the decision came from maneuvering between visible and invisible Actors. I would argue that the political dimension is prevalent in most large organizations and it is corrosive to the overall health of the organization. I would also argue that Steve Jobs designed Apple specifically to avoid the Political process. But we must still assume that it’s at work to some degree. It’s like entropy.

When hearing about big staff changes at Apple, take a moment to reflect what decision processes are at work. How did that one (visible) Actor really influence the decisions made? Are you ascribing too much to them because they are visible? Are you assuming that tens of thousands of other individuals are not influential? That they are minions hired to act and not to ask questions? Doesn’t Apple also say they hire people to tell Apple what to do?

Allison did not say which model applied to the Cuban Missile Crisis. He left it to the reader to decide.

I will do the same when it applies to any particular Apple decision.

The Apple Watch is now bigger than the iPod ever was. As the most popular watch of all time, it’s clear that the watch is a new market success story. However it isn’t a cultural success. It has the ability to signal its presence and to give the wearer a degree of individuality through material and band choice but it is too discreet. It conforms to norms of watch wearing and it is too easy to miss under a sleeve or in a pocket.

Not so for AirPods. These things look extremely different. Always white, always in view, pointed and sharp. You can’t miss someone wearing AirPods. They practically scream their presence.

For this reason wearers, whether they want to or not, advertise the product loudly. Initially, when new, they looked strange, even goofy. But the product’s value to the wearer overcame any embarrassment and for those courageous enough to wear them, they became a point of pride. As all things distinctive enough, the distinction rubs on the user and that distinction begets new users and new distinction, and so on. So now we have a bona fide cultural phenomenon.

I have both my son and parents angling to get these things. I have not seen this universal appeal recently, even for the watch. You have to explain the watch. The AirPods explain themselves. The only thing which AirPods do remind me of is the original iPod. The iPod-and-white-earbuds had a similar signal/function ratio. Looks distinctive, works well, nails the job to be done and is self-describing. The “iconification” of white was the phenomenon of its decade.

One wonders how much of this behavior is by design or, more precisely, engineered by designers. Did Jony Ive’s team plan on users “flexing” with their AirPods? Did they make them distinctive on purpose with the stalks pointing down vs,, for example, wrapping around the back of the ear for a more discreet look? Was it just good luck and the form followed function? It’s hard to imagine that taste could be engineered but here we are.

Whether planned or not, the newest AirPods offer a functional upgrade with no visual upgrade. This is noteworthy because whatever they got right with the original design they decided not to mess with it. You can’t tell if someone is wearing the newest AirPods or the originals.

As far as the added functionality it is typical Apple: faster connections due to a new chip, longer talk time, longer listen time, voice-activated Siri and wireless charging. Broadly speaking they are just better in ways that need to better and not better in ways they are good enough.

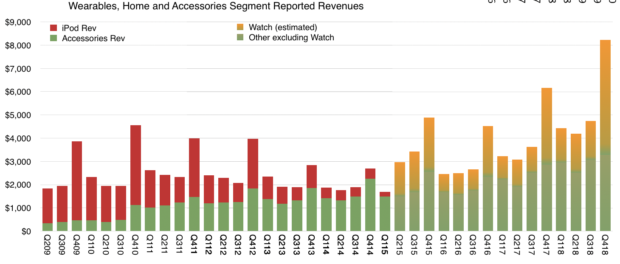

The product is part of the “wearables” category at Apple which includes watch and is growing almost 50%/yr. and not from a small base either. The following graph show the history of the segment since 2009 (before the iPod peaked).

As can be seen, Wearables and Home segment grew out of the iPod segment, through “Other” products and is now almost double what the iPod used to be alone.

It should be noted that the AirPods can be paired directly with the Apple Watch and used independent from the iPhone. If not from this point alone, culturally the iconic white AirPods and jewel-like Apple Watch embody the spirit of the iPod.

We want things to get better. The desire of improvement and an increase in performance is seemingly innate. The old adage goes that using the word “new” is the most effective way to increase sales. “New & Improved” if you want to be redundant.

For many in technology, New & Improved means faster with more of every measurable parameter. More memory, more pixels, more storage, more bandwidth, more resolution. In devices, the tendency has been to communicate “new & improved” through an increase in screen size. We are subject to this to such an extent that phones are becoming unusable with one hand, stretching screens to the edge of the device and then wrapping those screens around the edges and then even folding the screens so that we have to unfold or unroll to use the product. Maybe an origami phone is in the works.

But there is a parallel movement where “New & Improved” means smaller. This is the trend to miniaturization. Smaller is better because it’s more portable, more conformable. Things sold by the ounce are better than things sold by the pound. The best computer, the best anything, is the one you have with you and having it with you is more likely if you can take it with you. So that which you can take with you is the best. QED.

Apple has had a great history of miniaturization. The original Macintosh was tiny compared with personal computers of its day. It had a handle so you could take it with you. Apple pioneered laptops with breakthroughs in utility and form which made them truly portable. The iMac followed with a degree of integration and portability which made it iconic. Of course the iPod and iPhone were marvels when they first appeared.

Over the years these products expanded into ranges with “good, better, best” type segmentation. The bigger being the best in performance and the smaller typically being the most convenient. However it seemed that the positioning was toward “bigger is better” for a lot of these products. The iPhones Plus, the iPads Pro, etc. As even the largest were getting thinner, the “mini” versions appeared to be neglected. You could get “good enough” portability from the larger products so why bother with the minis.

It came to a head when the iPhone SE was discontinued last fall. Its demise felt like the end of an era. I always considered the SE as the “Steve Edition”. It was the last design Steve Jobs was involved in and it pained me to see it go. With it seemed to go the positioning around “mini”.

But also last fall we saw a re-boot of another almost-forgotten mini: the Mac mini. For me the Mac mini was quintessentially Jobsian. I remember that he loved tiny products. His launch of the iPod nano was spectacular; reaching into his jeans’ watch pocket to pull it out on stage. Holding the Mac mini up as if a tiny tray. Even the iPod shuffle was a quirky and lovable idea1. And let’s not forget the Mac Cube which made the iMac look huge.

When the Mac mini was released last fall in Brooklyn with a huge spec bump and a thunderous reveal I thought something was up. When the MacBook Air was also out at the same event I felt that the company was signaling something. Perhaps a re-dedication to the low end.

Also in parallel there is the wearables product line. The AirPods and the Apple Watch are jewelry. The essential qualities of products you wear are that they be small and beautiful. The smaller the better. Above all, both the Watch and AirPods are marvels of miniaturization. They pack so much in so little volume and that volume is shaped in such an aesthetically elegant way that they become daily essentials. I use my Apple wearables more than any other Apple product. Watch glances and time with AirPods exceeds the iPhone unlocks and iPhone use time. The fact that we don’t even realize that the smallest Apple products are also the ones we use most is a testament to their conformability to us.

So the Mac mini that is suddenly the Mac Maxi in performance, the MacBook which is an extraordinarily small laptop, the wearables success, all pointed in a direction that the iPhone did not: that “mini” was back.

And now we see the iPad mini being re-launched with a huge spec bump. We should take the hint. The iPad mini is just charming. I have been trying it out for a few days and it has worked its way into my routine. I have an iPad Pro that I use on a desk to design presentations (and to deliver them). I use it with a keyboard for dealing with email on my lap or on a plane and take it instead of a laptop when going to meetings.

But the iPad mini worked its way to my nightstand. It the one I reach for when on a couch. It is like an iPhone but when you’re at home it’s better than the iPhone because you can linger on that new true tone screen. It works well one handed. It now has Pencil support so it can be used for sketching and doodling.

I am an analyst not a product reviewer but I sense how it fills a gap between iPhones and larger devices–in a home setting. Of course it can be used in an office. It is much easer to take with you if you carry a laptop in a bag.

Fundamentally explaining mini is pointless. mini is something that is felt more than it is perceived. You can see the attraction of a tiny product only when you come face-to-face with it. In a picture it’s hard to get it–there is no frame of reference. What draws me to a MacBook or to a mini or a Watch is when it’s touched and held and carried or worn. The experience of the product is not how it works but how it works with you. You have to be part of it. It’s not asking “Does it look good?”. It’s asking “Does it look good on me?” mini means more personal.

That is the nature of mini and that is why I love the new minis: the iPad mini, the Mac mini, the MacBook (mini) and that is what I dare to hope that there is an iPhone mini coming.

probably the first Apple wearable as you could actually pin it to your clothes [↩]

In the latest Apple Earnings report, Apple announced a few details that are relevant to the forecast of the business:

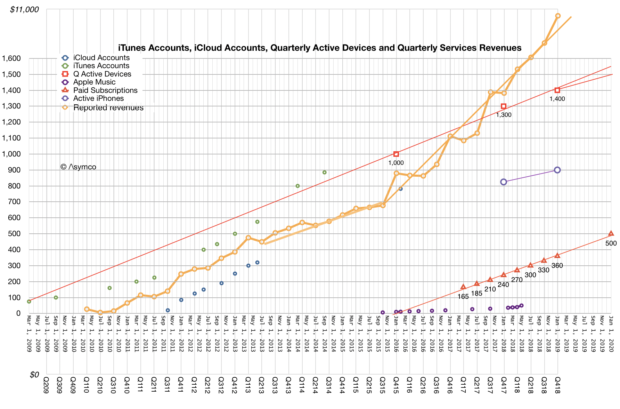

The global active installed base for iPhone reached an all-time high at the end of December, surpassing 900 million devices. This represents growth y-o-y in each of five geographic segments, and growth of almost 75 million in the last 12 months alone

There are now over 360 million paid subscriptions across the Services portfolio, an increase of 120 million versus a year ago. Apple expects to surpass 500 million in 2020.

The installed base grew to 1.4 billion devices by the end of December. This includes all-time highs for each of the main product categories and all five of their geographic segments.

I added all these data points to the previous reported figures related to installed base, subscriptions and Services revenue.

Note that all the data sets show a linear growth path. Most prominent is the paid subscriptions line which is growing at exactly 30 million per quarter. The new projection of 500 million by 2020 is exactly in-line with this projection.

Note also that active devices and iPhones are on similar trajectories. The figure for active iPhones is interesting because it very closely relates to active users. It’s extremely likely that 900 million active iPhones means 900 million active iPhone users. An iPhone is useful if it has a data plan associated and it’s a costly proposition for most people to have multiple devices and multiple data plans.

This close relationship between iPhone usage and iPhone users means that we can approximate the entire unique user base for Apple. There might be “10s” of millions of users who use Apple devices but don’t use iPhones but there might also be multiple iPhones for some users1

So it’s very likely that the total Apple user base is between 900 and 1 billion. If it’s not 1 billion now then it’s very likely it will be 1 billion within 12 months.

In May 2010 I made the prediction that Apple would reach a billion users in 5 to 8 years. The prediction was based on the first 100 million iOS users. The company reached one billion active devices in a bit over 5 years and is about to reach 1 billion users 8 years since.

Apple stated in the latest conference call that very little of Services revenues depends on the any previous quarter’s unit sales confirming that Services is driven almost entirely from the user base. With almost a billion users, 90+% loyalty rate, 95% satisfaction, 120 million paid subscriptions and 75 million new users/yr, the analysis of Apple as a services company is becoming interesting.

I would be inclined to assume that there are more non-iPhone Apple users than multiple iPhone users. [↩]

For the last two years I’ve been studying the transportation economy and introducing the idea of Micromobility. Simply, Micromobility promises to have the same effect on mobility as microcomputing had on computing. Bringing transportation to many more and allowing them to travel further and faster. I use the term micromobility precisely because of the connotation with computing and the expansion of consumption but also because it focuses on the vehicle rather than the service. The vehicle is small, the service is vast.1

One of the elements of analysis for Micromobility is the notion of Unit Economics. The idea is that each vehicle can be seen as an independent business. It requires an investment, has a revenue attached, requires operating costs and fixed costs and finally, hopefully, generates earnings. A fleet’s economics is therefore a multiplication of the unit economics by the fleet size. A similar partial construct exists for mobile network operators where the network revenue is defined by ARPU (average revenue per user). In consumer hardware we also have the idea of ASP (average sales price) and BOM (bill of materials) which describe the revenue and variable cost of each device.

In the case of Micromobility the unit economics is more broadly applied in being an entire P/L statement for each vehicle. One example for the e-scooter sharing company Bird is here. If the unit economics of Bird is consistent across geography and time then the entire business can be valued based on one “average unit”. Measuring the health of the business can thus be summarized in BOM, Utilization, Lifespan, Attrition and Cost structure or one unit.

For some time now I’ve advocated a similar approach for Apple.

If you want to learn about the real future of transportation sooner rather than later, do consider coming to the Micromobility California conference. [↩]

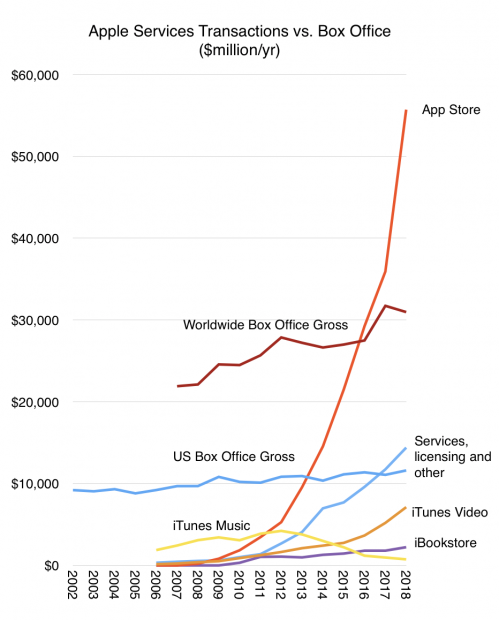

In June of this year Apple reported that it had paid a total of $100 billion to developers. That is the 18th such figure given in the 10 year history of App Store, making the progress of payments and hence revenue and spending easily trackable.

The other regularly reported figure is the business segment revenue where App sales are currently allocated. Now called “Services” this omnibus segment includes many other sources of revenues such as:

Digital Content (Books, Music downloads, Video downloads–including TV shows and movies and movie rentals.)

AppleCare, Apple’s extended warranty service.

Apple Pay, transaction fees

Apple Pro Apps, including Final Cut, Logic Pro, Motion, Aperture

Licensing including “Made for iPhone/iPad”

One-time settlements of various lawsuits.

Other Services revenues which include

Apple iCloud-related services

Music Match

Music subscriptions

Other third party subscriptions (commissions)

Third party licenses

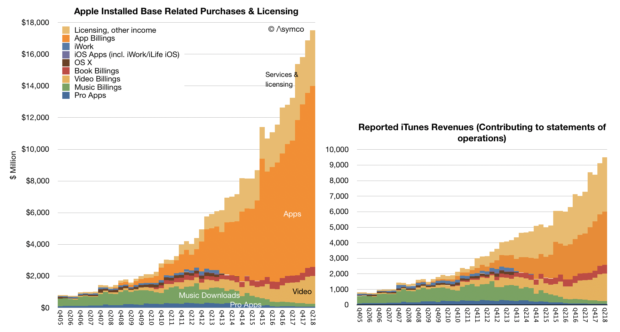

This combined Services segment is significant with $35 billion revenues in the last 12 months. This is quite a jump from 2016 when Services had crossed $25 billion. At the end of 2016 Apple said it expected Services revenue to double by 2020. With a growth rate since then of 25% the company is on track to reach its target one year early.1

Consumer spending on Apple services includes more than what it books as revenue since only the (typically) 30% of App Revenues is considered Apple’s revenue. Including the payments to developers, Services generated over $65.5 billion/yr in billings. This will reach $100 billion/yr in 2 years. The difference between reported revenues and consumer spending is shown in the following graphs.

I described the visibility into App Store revenues (which is the orange area in the graphs above) but the other sub-segments of Services are much more difficult to ascertain. Of special interest is Other Services which includes very high margin services. As part of that there is a peculiar source of revenues: Google.

It’s known that Google pays Apple for the default placement of Google search within Safari on iOS and Mac OS. That payment is registered by Google as a “Traffic Acquisition Cost” or TAC. TAC is essentially payment for distribution where what is granted by the distributor is access to queries (traffic.) This way Apple acts as distributor for Google. So, for that matter, does Firefox which also receives TAC payments.

What is peculiar is that the amount of TAC paid by Google to Apple is becoming staggering.

A few years ago Google was paying over 20% of its revenues as TAC. Recently that ratio rose to 23%. Bernstein analyst Toni Sacconaghi estimated that Google paid Apple $1 billion in 2014 as TAC and that payments to Apple were about $3 billion in 2017. Now Goldman Sachs analyst Rod Hall estimates Google could pay Apple $9 billion in 2018, and $12 billion in 2019.

This is starting to look interesting but is it believable?

My own estimate of Apple’s Other Services (which includes TAC revenues) is a run rate of $15 billion for calendar 2018. This makes $9 billion (60%) from Google quite challenging but not impossible. The remaining $6 billion needs to account for Apple’s own cloud and subscription service revenues.

Does this make sense given Google’s spending? TAC payments to distribution partners in Q2 were $3 billion. The $9 billion/yr assumption implies a $2.25B/quarter payment to Apple. That would be 75% of Google’s distribution costs. That also sounds reasonable given the high utilization of iOS relative to any other platform.

An increase to $12 billion for next year is also quite a claim but it certainly is possible. I don’t have a basis for making this estimate but the assumption of growth leads me to conclude that the payments are tied to actual traffic generated.

In other words the two companies have an agreement that Apple is paid in proportion to the actual query volume generated. This would extend the relationship from one of granting access for a number of users or devices to revenue sharing based on usage or consumption.

Effectively Apple would have “equity” in Google search sharing in the growth as well as decline in search volume.

The idea that Apple receives $1B/month of pure profit from Google may come as a shock. It would amount to 20% of Apple’s net income and be an even bigger transfer of value out of Google. The shock comes from considering the previously antagonistic relationship between the companies.

The remarkable story here is how Apple has come to be such a good partner. Both Microsoft and Google now distribute a significant portion of their products through Apple. Apple is also a partner for enterprises such as Salesforce, IBM, and Cisco. In many ways Apple is the quintessential platform company: providing a collaborative environment for competitors as much as for agnostic third parties.

To calibrate this consider that Facebook revenues for the last 12 months were $48 billion and it now has a market capitalization of $468 billion or 41% that of Apple whereas Services consists of about 14% of Apple’s total revenues. [↩]