Apple reports second calendar quarter results in about a week. I propose the following estimates:

Fiscal Q3 2017:

Rev ($B) 45.321

EPS ($) 1.62

iPhone (units) 41 million

iPad (units) 9.8 million

Mac (units) 4.35 million

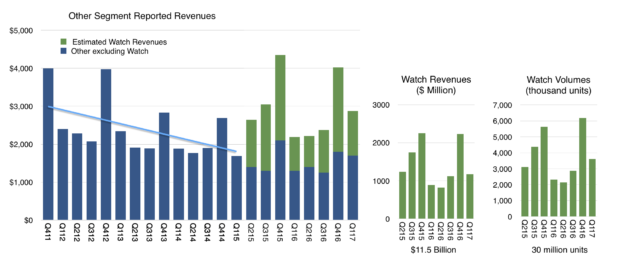

Watch (units) 2.5 million

Services ($) 7.2 billion

Other products ($) 2.6 billion

Gross margin (%) 38.4

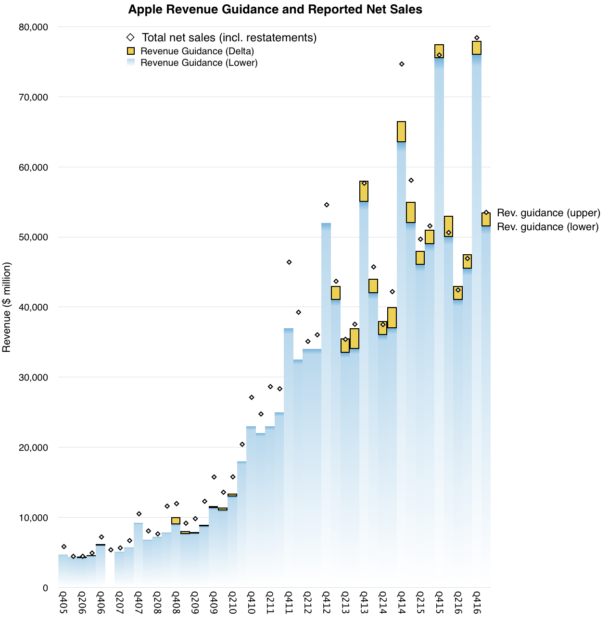

The revenue estimate is visualized in relation to guidance (revenue between $43.5 billion and $45.5 billion) and shown in the context of previous actual revenues below:p

The estimates are also consistent with additional guidance provided:

- Gross margin between 37.5% and 38.5%

- Operating expenses between $6.6 billion and $6.7 billion

- Other income/(expense) of $450 million

- Tax rate of 25.5%

The estimates (and guidance) suggest modest growth of 7% in revenues and 13.7% EPS. The predictability of the quarter suggests that attention will mostly be focused on guidance for the next quarter.

Expectations can vary quite a bit because of the effects of a new launch. The product mix, pricing and timing are all unknown at this time.

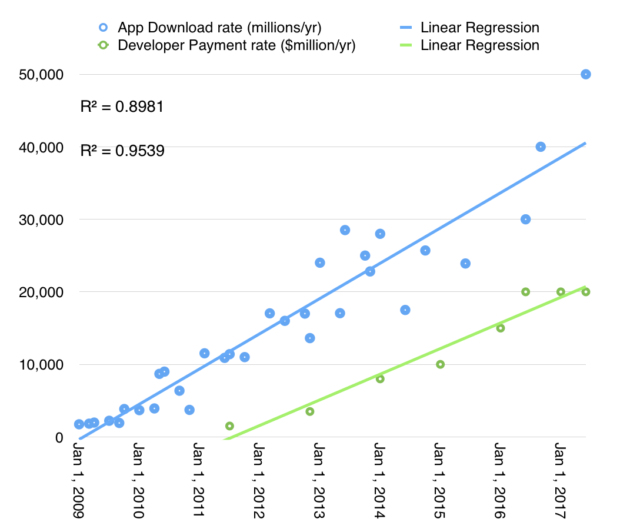

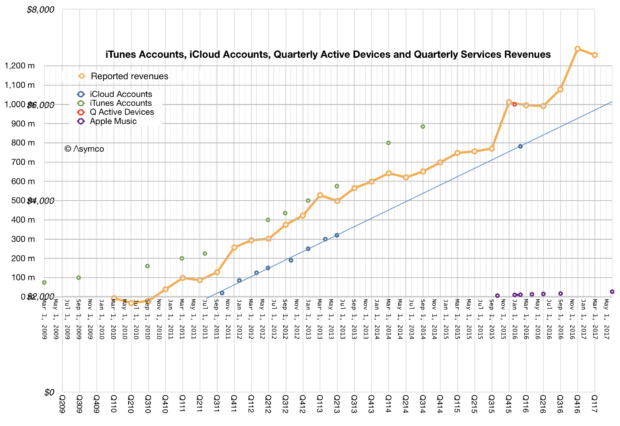

What is known however is that the customer base for Apple is increasing and loyalty is higher than ever. What I sense, coming from very few data points, is that there are more iPhones in use than ever before. A few years ago when the market was less saturated it was easy to assume that commodity Android phones and tablets would surge and swamp iPhone/iOS usage.

This has not happened, indeed the data suggests that iOS usage is stronger than ever and that there are many more “switchers” moving from Android to iOS than vice-versa.

This may surprise some but if we look at the PC market, a similar phenomenon has been taking place for years. Mac usage grows and Macs are more visible and valuable than PCs.

It’s important to note that in the latter, post saturation stages, the markets for both phones and computers are increasingly driven by brand value. This resistance to commoditization is due to buyers’ perceptions of quality moving beyond utility and of the prioritization by buyers of new measures of performance. These new measures defy measurement.

Much of what is therefore required of market analysts is intuition.