We’ve sold well over 3 million since we launched it 3 weeks ago

via Live from Apple’s iPhone 4 press conference — Engadget.

Could we dare to think that implies 52 million in a year’s production?

Mobile Computing Industry

We’ve sold well over 3 million since we launched it 3 weeks ago

via Live from Apple’s iPhone 4 press conference — Engadget.

Could we dare to think that implies 52 million in a year’s production?

Sony Ericsson shipped 11 million phones at an average selling price of EUR160 in the second quarter, compared with 13.8 million units at an average price of EUR122 a year earlier. Sales rose to EUR1.76 billion from EUR1.68 billion, against expectations of EUR1.79 billion.

The company’s estimated share of the global handset market remained flat from the previous quarter at around 4%.

The company reported net profit of EUR12 million for the three months to June 30, compared with a EUR213 million net loss the year before, missing analysts’ expectations for a EUR50 million profit but sustaining the turnaround that started in the first quarter.

via Sony Ericsson Swings To 2Q Profit.

Sony Ericsson still sells more phones than Apple.

See also:

One of the biggest losers in the Kin debacle that hasn’t been talked about is Sharp. OEM for the Kin, and the biggest cellphone brand[s] in Japan….but not in the states of course. Kin was supposed to be their entry point into the US market for mobile. Sharp ponied up half the ad $$ for the Kin launch…basically subsidised it with the thought it would be good for their brand and they would sell a lot of phones and be a trojan horse for other Sharp Mobile efforts in the US. Big fail. Not only did they have to tool up factories custom design hardware and sub the marketing they only sold a few thousand phones at best. Sharp’s taking a huge bath on this one. And because Sharp’s mobile group is in Nara Japan and had no people on the ground in WA or Palo Alto…they had little leverage or insight into the US market and got taken for a ride. I’m sure there are a lot of unhappy execs in Osaka right now cause of this…

via Mini-Microsoft: The KIN-fusing KIN-clusion to KIN, and FY11 Microsoft Layoff Rumors.

That link leads to over 600 comments from Microsoft employees regarding the Kin fiasco. Eye watering.

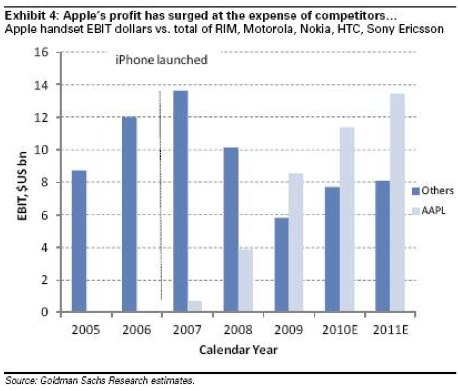

Apple will generate 2X as much handset profit as the rest of the industry combined this year DESPITE SELLING ONLY 3% OF THE HANDSETS BY UNIT VOLUME

That interpretation of the data is exaggerated and/or incorrect. An analysis of profitability was done with respect to Nokia here and industry-wide here.

Goldman Sachs analysis (graph below) shows competitors’ profits and losses combined. Sony Ericsson and Motorola generated negative profits during 2008 and 2009 and may do so through 2010. Apple’s profits are likely to be larger than the industry *net* profits but not twice as much by 2011 (the graph does not even show that; 13.5 is not twice 8). Furthermore, the competitors do not include Samsung and LG!

Exaggeration or not, the fact remains that Apple entered the market in 2007 and in only three years became the most profitable phone vendor. It’s indicative of the value of an integrated user experience innovation in the market, which itself is indicative of the value of software in a hardware-oriented incumbency.

When the Kin was launched, many, including myself, were skeptical. It was a product that contradicted much of what made sense in the industry. It was not a smartphone, it was not a platform and it was predicated on a niche use case. It was, in essence, a feature phone, and as such was not differentiable. However, most people, myself included, were willing to overlook some of these flaws on the basis that Microsoft *must* have done some rigorous product research to support this concept. We fell for the premise that the Emperor *must* have been wearing clothes.

It turns out he wasn’t. With this knowledge, we should ask the same question regarding clothing to the “next of kin”: Windows Phone 7. There is this same sense of deja vu, that there are a lot of things wrong with WP7, but Microsoft can’t be foolish enough to fail on this. The problems with WP7 are indeed potentially fatal:

– It is a new platform with no ecosystem facing entrenched incumbents

– It is expensive relative to Android for OEMs while being completely symmetric in its approach to the licensing market

– It is not leveraging the installed base of Windows Mobile, and is alienating to WM’s core business users/buyers.

– it faces a branding challenge, like its predecessor

– it is feature incomplete, barely on par with iPhone from 2008

In fact, it’s hard to come up with any key value upon which to anchor the platform. Beside the fact that it is new or, if one were charitable, “fresh” in the interface, it seems to be a solution looking for a problem. Reminiscent of the Zune in many ways, it’s tempting to dismiss it.

Yet there is always the benefit of doubt being from Microsoft. Or is there? After Kin, is it time to give up on the old adage that Microsoft persists until it wins and never gives up? The Microsoft that won was a low-end disruptor. Offering less-than-good-enough products at lower prices or bundling parts of software into compelling packages, Microsoft expanded markets and increased computing consumption. This is not in the cards for mobile computing.

Microsoft in Mobile is not playing to its core strengths. Indeed, mobility is a disruptive force for their core. Doing “the right thing” in mobile cannot but threaten the sustaining cash cow of Windows. Microsoft seems to be floundering precisely because it’s trapped in the innovator’s dilemma.

2010.Realization that iPhone is a threat from new dimensions (user experience). Planning begins on reshaping the software base as a market-driven (not technology-driven) asset (5 year cycle). Apple begins to be evaluated as a competitor in devices and services, although still not compliant with current market definitions.

via asymco | Assessing Nokia’s Competitive Response.

I wrote these words a year ago based on observations made three years ago. My expectation was and still is that Nokia does not quite understand what they are competing for and what the competition actually consists of.

On Friday Anssi Vanjoki wrote that “The fightback starts now.” He seems to contradict my timeline which has the “fightback” starting in 2014.

How do we settle this? Let’s turn to the claims:

In the article he says they sell 2 in 5 smartphones on the planet, yet, he turns around and says that Nokia is now the challenger in that space. He says Symbian is the way forward on smartphones, yet he says MeeGo is the way forward on ‘connected devices’. He writes that he is obsessed with getting Nokia to being number one in high-end devices (presumably by volume or sales or profit) but a recent survey by third-party tool developer Appcelerator shows 90 percent of developers surveyed said they were interested in the iPhone while 81 percent expressed interest in Android; for Symbian and MeeGo, the related figures were only 15 percent and 11 percent, respectively.

I’m not ready to revise my timeline. The fightback begins in 2014.

In June 2008, Nokia made its first big move to turn around the platform, and announced that it was acquiring Symbian, with the intent of turning the OS into an open source project.

Two years later, the move to open source has proved to be a miscalculation that is slowing down Symbian’s development. It would be better for Nokia to take full control of the OS, according to Wood. A lack of support from other vendors means Nokia has to do most of the work itself, while the open nature of the platform allows competitors to keep a close eye on its progress.

via Nokia on long comeback trail after smartphone misses – Digital Lifestyle – Macworld UK.

Then there’s LiMo foundation open source mobile Linux. Maemo is/was open source, Openmoko and Qt Extended and PalmSource/Access moving to open source and there was the Motorola Linux OS that launched years ago. If Open always wins, whatever it wins, it’s not market share.

Much has been made of the potential for Android to reduce the growth of iPhone. The iPhone seems to be doing very well and continuing to be supply rather than demand constrained.

RIM however seems to be under significant pressure. A Goldman Sachs analyst first pointed this out in her last report and placed a “Sell” on RIMM. The fact is that most of RIM’s sales are in the US on the carriers other than AT&T. In those very same carriers, Android is being pushed hard as a customer retention strategy, so iPhone is pressuring RIM only indirectly through Android.

The evidence is also in survey data. In the graph below, we see how iPhone buyers are considering Android as the most credible alternative to the iPhone whereas they considered BlackBerry the best alternative a year ago. In terms of vendors, what RIM lost HTC gained.

One can only wonder what will happen when the iPhone enters unrestricted distribution in the US. The results in other markets speak for themselves.

AppleInsider | Apple’s recurring revenue stream: 77% of iPhone 4 sales were upgrades.

Adding this all up, Microsoft has several mobile OS products in various stages of production, including

- Windows Mobile 6.5

- Windows Phone 7

- KIN

- Windows Embedded Handheld

- Windows Embedded Handheld 7

- Windows Embedded Standard 7

- Windows Embedded Compact 7.

As ZD blogger Mary Jo Foley noted recently, this fact is somewhat amusing in the wake of Microsoft CEO Steve Ballmer’s criticism of Google for having two different mobile OSes (Chrome OS and Android.)

via Microsoft’s Mobile Strategy Isn’t A Strategy. It’s A Mess.

That’s not version 7 of an OS, that’s 7 different OS’s in the market at the same time.

RIMM shares dropped more than 5% after hours after company reported “light” units and a 20% rise in profit with a 24% rise in revenue.

RIMM sold 11.2 million units (of which 4.9 million were new subscribers and the rest replacement units–a deterioration in replacement rate). This represents 43% growth. The unit growth is nearly double the revenue rise implying a lower ASP ($300–half the iPhone) and margin (45.4%).

RIM passed another milestone: 100 millionth BlackBerry was sold during the quarter. We’ve noted before that Apple will also pass its 100 millionth iOS device this month. RIM sold 20 million units as of October 2007, right on the heels of the iPhone launch. That means that iOS grew 100 million to BlackBerry OS growing 80 million in the same time frame.

So why are shares at a P/E of 13? 20% EPS growth would be respectable numbers, but the smartphone market is growing faster than that. The implication is that RIMM is losing share and everyone is expecting that loss to accelerate.

Simona Jankowski from Goldman Sachs repeats her Sell rating. “RIM has now missed top-line expectations for three of the last four quarters, in our view demonstrating the building competitive pressures on its business from the iPhone and more recently from Android,” she writes. “We estimate that net subscriber additions in North America declined on a sequential basis, which we attribute primarily to the success of Android-based phones, such as the Motorola Droid and the HTC Incredible at Verizon.”

Research In Motion Limited (USA): NASDAQ:RIMM quotes & news – Google Finance.